Table of Contents1. Introduction |

|

Introduction

Filing GST returns every month looks very simple to think but many businesses face difficulties between the data reported in GSTR-1 and GSTR-3B. Even small errors can create large compliance issues, tax notices and unnecessary interest liability.

Understanding the GSTR-1 and GSTR-3B mismatch reasons is important for you if you want to maintain accurate tax records and make sure smooth GST compliance. When sales details and tax payments do not match it raises red flags in the GST system. In this blog, we will explain why mismatches happen, how they affect your business and what steps you can take to correct them properly.

What is GSTR-1 and GSTR-3B?

GSTR-1

GSTR-1 is a detailed return that contains invoice-wise information of all outward supplies (sales). Businesses report taxable value, GST rate, tax amount and customer GSTIN details. Then the information filed reflects in the buyer’s records and helps them to claim input tax credit.

GSTR-3B

GSTR-3B is a summary return where total sales, tax liability and input tax credit are declared. Based on this return, the taxpayer pays the net GST amount to the government. It does not require invoice-level data but must match the details already reported in GSTR-1.

In simple terms, GSTR-1 shows detailed transaction data while GSTR-3B shows the summarized tax liability and payment. If both returns show different values then it results in inconsistencies.

Why Matching GSTR-1 and GSTR-3B is Important

Matching both returns is not just a requirement, it is a necessary compliance step. When there is a difference between the two, the GST department may issue a notice to ask for clarification. Regular reconciliation helps you to maintain transparency, correct tax payment and smooth return processing.

Here are some of the important reasons why matching both returns matters:

-

● It helps you make sure that the tax liability declared in GSTR-3B is fully supported by invoice details reported in GSTR-1.

-

● It reduces the risk of departmental notices and audit queries.

-

● It prevents short payment or excess payment of tax due to reporting errors.

-

● It helps to maintain proper records for annual returns and GST audits.

-

● It protects customer relationships by making sure that the ITC reflects accurately in their returns.

-

● It supports GSTR mismatch penalty avoidance by identifying issues early and correcting them on time.

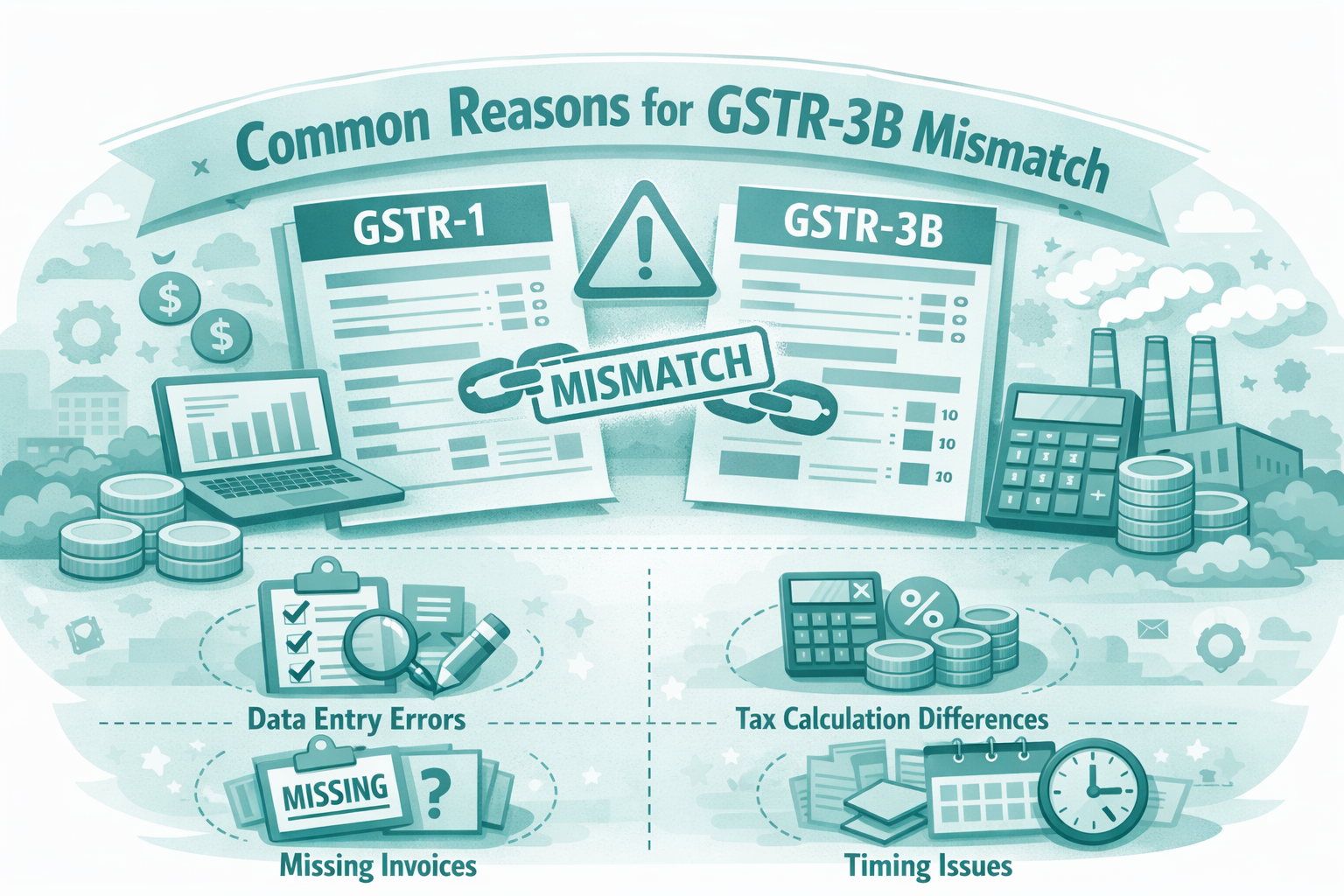

Common Reasons for GSTR-1 and GSTR-3B Mismatch

There can be several GSTR-1 and GSTR-3B mismatch reasons that businesses commonly experience. So Let’s understand them in detail:

1. Sales Reported in GSTR-1 but Not Included in GSTR-3B

Sometimes invoices are uploaded correctly in GSTR-1 but the total taxable value is under-reported in GSTR-3B due to manual calculation errors.

2. Incorrect Tax Calculation

Applying the wrong GST rate or making arithmetic mistakes while creating GSTR-3B can create differences in tax liability.

3. Amendments Not Updated Properly

When corrections are made in GSTR-1 but the changes are not adjusted in GSTR-3B then mismatch occurs.

4. Timing Differences

A transaction may be recorded in GSTR-1 of one month but reported in GSTR-3B of another month which causes temporary variance.

5. Credit Notes and Debit Notes Errors

If failure to report credit or debit notes consistently in both returns, it can lead to differences in taxable turnover.

6. Wrong ITC Claim in GSTR-3B

Incorrect input tax credit claims or failure to reverse ITC properly can disturb return alignment.

7. Manual Data Entry Issues

Manual work increases the chances of duplication, omission or typing mistakes. Using GST reconciliation software for GSTR-1 and GSTR-3B helps to minimize such risks.

Understanding such issues allows businesses to apply the right GSTR-1 and GSTR-3B mismatch solution without delay.

How to Reconcile GSTR-1 and GSTR-3B

If you are wondering how to fix GSTR-1 and GSTR-3B mismatch, the solution is to do systematic reconciliation before filing returns every month.

Many businesses now use a GSTR-1 GSTR-3B reconciliation tool to automate the comparison process. Advanced GST filing software with mismatch detection highlights differences instantly and reduces manual effort.

Here are some practical steps you can follow:

-

● Compare total outward supplies reported in GSTR-1 with taxable turnover declared in GSTR-3B.

-

● Verify tax liability calculations before making payment.

-

● Check credit notes, debit notes and amendments carefully.

-

● Review ITC claims with purchase records and GSTR-2A/2B.

-

● Maintain proper documentation for adjustments and corrections.

-

● Reconcile data internally before final submission.

Conclusion

Mismatch between GSTR-1 and GSTR-3B is common but it should never be ignored. Even small differences can result in notices, penalties or interest liability if not corrected on time.

By understanding the root causes and implementing proper reconciliation practices you can avoid compliance stress. Regular review, accurate reporting and the right technology support play a major role in maintaining smooth GST operations.

When returns are filed carefully and reconciled every month businesses not only avoid legal issues but also build a strong foundation for long-term financial stability.