Table of Contents

|

|

Introduction

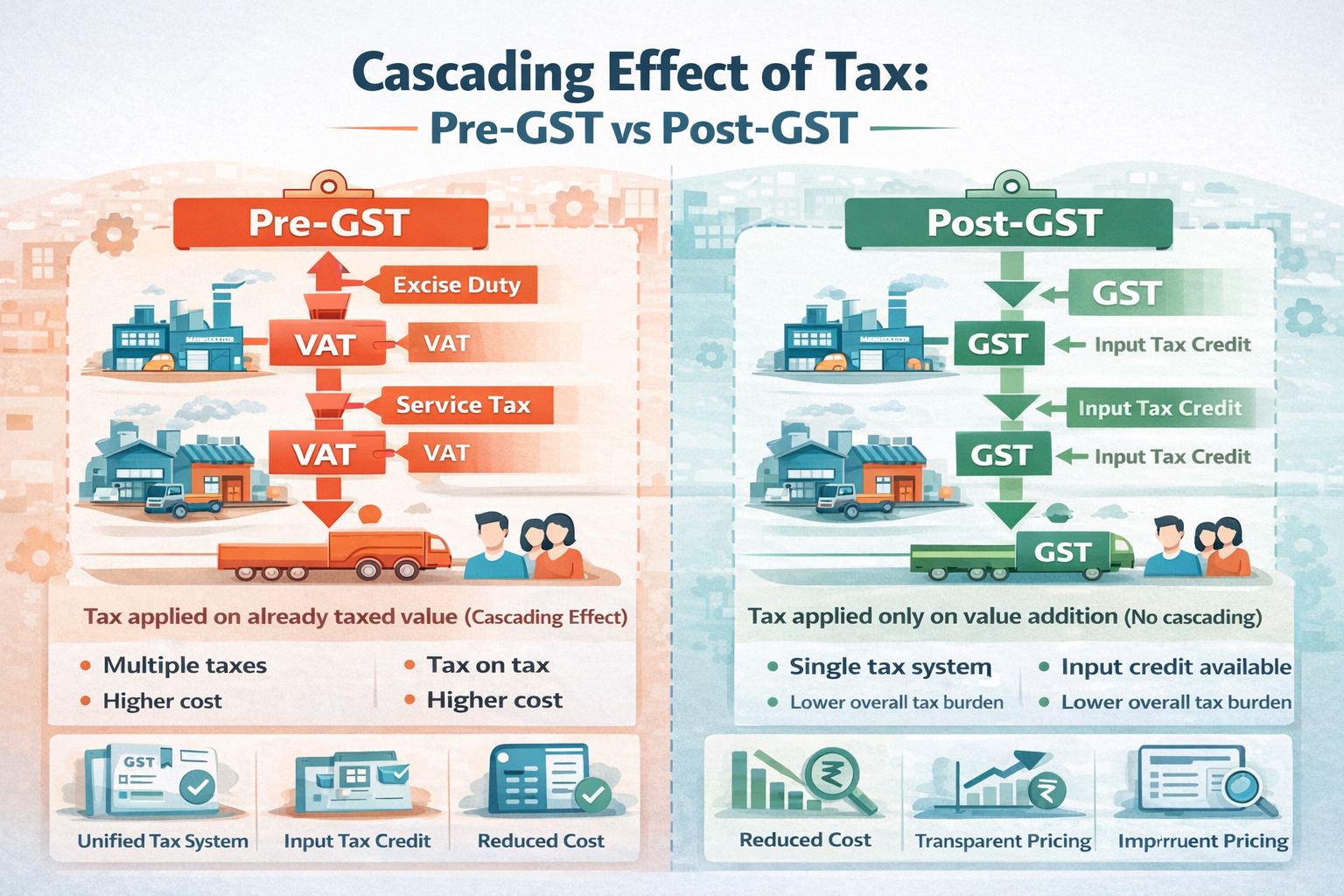

Businesses had to deal with multiple indirect taxes such as excise duty, VAT and service tax before GST was introduced in India. These taxes were applied at different stages of production and sale. Because of this a product was taxed more than once before reaching the final customer.

This repeated taxation is known as the cascading effect of tax. It used to increase the final price of goods and made the taxation system complicated for businesses. One of the main goals of GST was to reduce this issue.

What is Cascading Effect of Tax

Cascading of tax means a situation where tax is charged on a value that already includes tax paid earlier.

In other words, tax on tax is called the cascading effect because the tax is calculated on an amount that already includes previous taxes.

For example, a manufacturer pays tax when producing goods. When the same goods are sold to a wholesaler another tax is applied on the total price that already includes tax. And when the retailer sells the product to the customer then the tax may again be applied on the updated price.

Cascading Effect of Tax in the Pre-GST System

India had several indirect taxes used to be applied separately before GST. These taxes were applied by both central and state governments which created multiple layers of taxation in the supply chain.

-

● Excise duty was charged during manufacturing

Manufacturers had to pay excise duty to the central government when goods were produced, which used to increase the base cost of the product.

-

● VAT was applied when goods were sold

When the same goods moved to wholesalers or retailers, VAT was applied on the selling price that already included excise duty.

-

● Different taxes applied by different authorities

Businesses had to pay taxes like service tax, entry tax and VAT which used to depend on the nature of the transaction.

-

● Limited ability to claim tax credits

Businesses could not always claim credit for taxes paid earlier under different tax systems.

-

● Increase in product prices

Because taxes were repeatedly added at different stages the overall cost of goods increased significantly.

How GST Removed the Cascading Effect of Tax

GST was introduced as a unified tax structure in India and it helped businesses to claim input tax credit for taxes paid earlier in product manufacturing to sales process. This system helped to reduce the problem of cascading effect in gst and helped to make sure tax is applied only on the value added at each stage. Some of the key points are given below on how it removed cascading effect:

-

➜ Businesses can now claim input tax credit on taxes already paid on purchases.

-

➜ GST replaced many indirect taxes and created a single tax system.

-

➜ Now Tax is applied only on the value added during each stage of production or sale.

-

➜ It improved transparency in tax calculation and reporting.

-

➜ Businesses across different states can now follow a more uniform taxation system.

-

➜ It helped to reduce repeated taxation in the supply chain.

Benefits of Removing the Cascading Effect

Removing repeated taxation has helped businesses to improve the efficiency of the tax system in India. It has also made pricing more affordable for consumers.

-

➜ It reduces the overall tax burden on products and services.

-

➜ Businesses can better manage their tax credits and financial records.

-

➜ Prices become more stable for customers.

-

➜ It simplifies tax compliance for businesses operating in multiple states.

-

➜ Supply chains become more transparent.

-

➜ It helps to reduce some negative effects of taxation that previously increased product costs.

Conclusion

The earlier tax structure created multiple layers of taxation that increased the cost of goods. Taxes applied at different stages resulted in repeated taxation and higher prices.

With the introduction of GST, the system shifted toward value-based taxation where businesses can claim credit for taxes already paid. This helped to reduce unnecessary tax burdens and makes the overall tax structure simpler and more helpful for businesses and consumers.